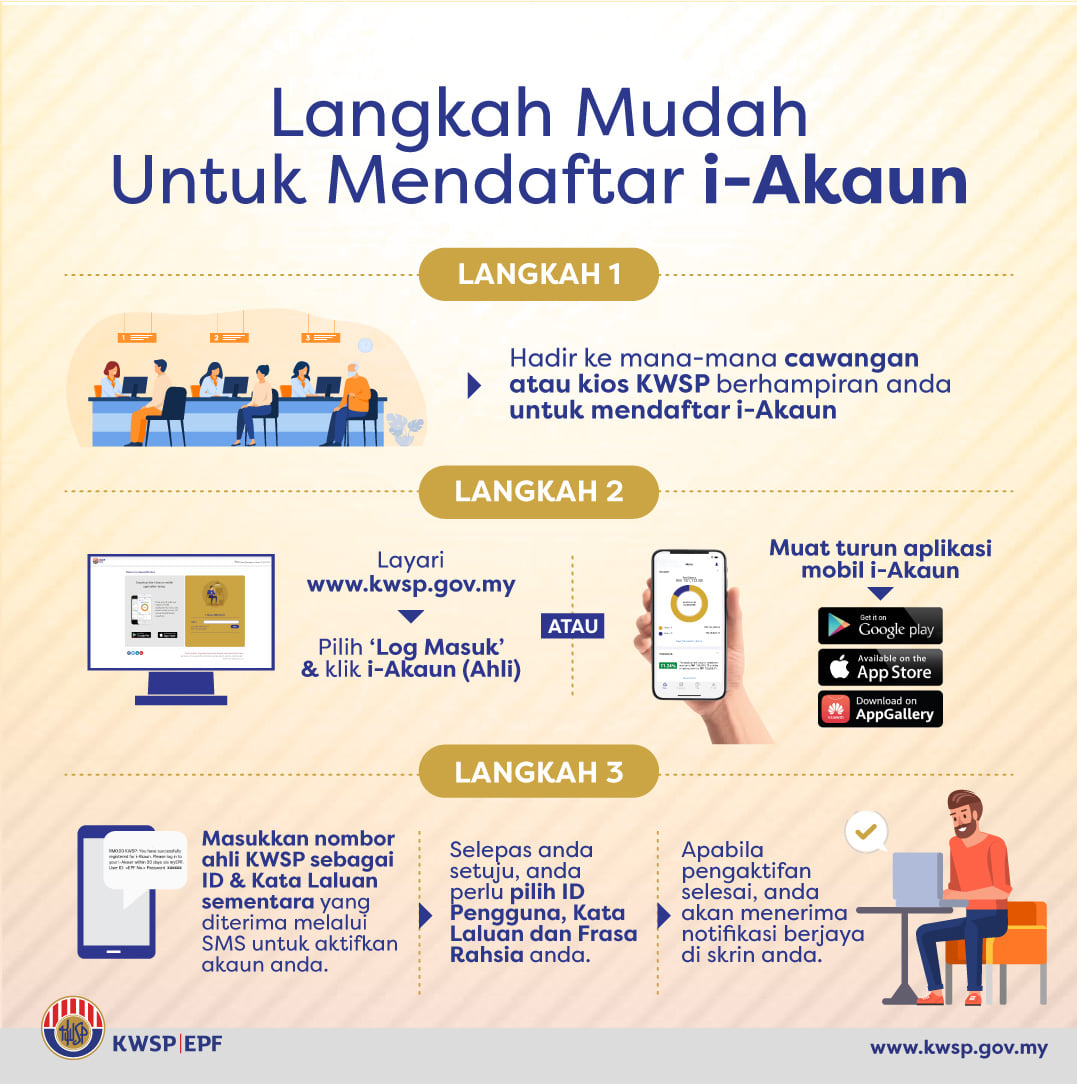

Unlocking Your Savings Potential: A Guide to Account 3

Planning for a secure retirement is a journey, not a destination. It requires careful consideration and strategic management of your finances. In Malaysia, the Employees’ Provident Fund (EPF) plays a crucial role in helping individuals build a solid financial foundation for their post-retirement years. While many are familiar with the basic structure of EPF accounts, Account 3 often remains an untapped resource. This account offers a unique opportunity to amplify your savings and secure your financial well-being in the long run.

So, what exactly is Account 3, and how can it benefit you? In simple terms, it’s an avenue within your EPF savings that empowers you to take greater control of a portion of your retirement funds. It provides flexibility, allowing you to invest a portion of your savings to potentially grow at a faster rate compared to traditional EPF returns.

The concept of Account 3 emerged from the recognition that individuals have varying financial goals and risk appetites. It acknowledges that a one-size-fits-all approach to retirement savings may not be suitable for everyone. By allowing members to invest a portion of their savings, Account 3 encourages financial literacy and active participation in shaping one's financial future.

Navigating the complexities of retirement planning can feel overwhelming at times. That's why understanding the nuances of Account 3 and its potential benefits is crucial. Whether you're seeking to supplement your retirement income, achieve specific financial goals, or simply make your money work harder for you, Account 3 can be a valuable tool in your financial arsenal.

However, it's important to acknowledge that investing always involves a certain level of risk. While Account 3 offers the potential for higher returns, it also comes with the responsibility of making informed investment decisions. It's essential to thoroughly research investment options, understand your risk tolerance, and consider seeking guidance from qualified financial advisors to make the most of this opportunity.

Advantages and Disadvantages of Account 3

Here are some potential advantages and disadvantages of Account 3:

| Advantages | Disadvantages |

|---|---|

| Potential for higher returns compared to traditional EPF savings. | Investment risk: Returns are not guaranteed, and you could lose money. |

| Flexibility to choose from a wider range of investment options. | Requires financial literacy and investment knowledge to make informed decisions. |

| Opportunity to grow your retirement savings more aggressively. | Time commitment required to research and manage investments. |

Best Practices for Utilizing Account 3

Here are some best practices for effectively utilizing Account 3:

1. Start early: The power of compounding can work wonders for your investments. The earlier you start, the more time your money has to grow.

2. Diversify your investments: Don't put all your eggs in one basket. Spread your investments across different asset classes to mitigate risk.

3. Review your portfolio regularly: Market conditions and your financial goals change over time. Regularly review and adjust your portfolio accordingly.

4. Seek professional advice: If you're unsure about investment options or need personalized guidance, consult a qualified financial advisor.

5. Invest for the long term: Retirement planning is a marathon, not a sprint. Stay focused on your long-term goals and avoid making impulsive investment decisions based on short-term market fluctuations.

Frequently Asked Questions about Account 3

1. How do I open an Account 3?

You don't need to open a separate account. It's automatically created within your EPF account.

2. How much can I contribute to Account 3?

There are specific limits on how much you can transfer from your Account 1 to Account 3. These limits are subject to change and can be found on the official EPF website.

3. Can I withdraw from my Account 3 before retirement?

Withdrawals are generally allowed for specific purposes, such as housing or medical expenses. However, restrictions apply, and it's essential to check the latest guidelines.

4. What are the investment options available for Account 3?

You can choose from a range of unit trust funds, private retirement schemes (PRS), and other approved investment products.

5. Is my money in Account 3 safe?

The safety of your investments depends on the performance of the chosen investment products. It's crucial to understand that investments carry risk.

6. What happens to my Account 3 when I retire?

You can choose to withdraw the funds or continue investing.

7. Where can I find more information about Account 3?

Visit the official website of the Employees' Provident Fund (EPF) or consult a licensed financial advisor.

8. Are there any fees associated with Account 3?

Fees and charges may apply depending on the investment products you choose. Check with your chosen investment provider for details.

Tips and Tricks for Maximizing Account 3

Consider setting up automatic monthly transfers to your Account 3 to make investing a consistent habit. Regularly track the performance of your investments and don't be afraid to adjust your strategy as needed.

In conclusion, Account 3 offers a powerful avenue for individuals to take charge of their retirement savings and potentially grow their wealth beyond traditional methods. While it's essential to approach investments with careful consideration and a long-term perspective, understanding the nuances of Account 3 can empower you to make informed decisions and pave the way for a more financially secure future. Take the time to explore the available options, assess your risk tolerance, and consider seeking guidance from qualified financial professionals to embark on this exciting journey toward a fulfilling retirement.

Gacha life characters unleashed exploring the world of customizable avatars

Back of hand tattoos a bold statement or a regret waiting to happen

Unveiling the legacy exploring the world of johnnie walker whisky

{kind=link}