Received a Check From Wells Fargo? What You Need to Know.

We live in a world increasingly dominated by digital transactions, a world of Venmo, Zelle, and instant transfers. Yet, sometimes, the old ways persist. Sometimes, you open your mailbox to find a tangible piece of finance – a check – and not just any check, but one from Wells Fargo. This unexpected arrival prompts a series of questions. Is it legitimate? What does it mean? How should you proceed?

The experience of receiving a check from Wells Fargo, or any financial institution for that matter, is more than just a simple transaction. It's a tangible reminder of financial dealings in a digital age. It can be a source of excitement, confusion, or even concern depending on the context. This check, a symbol of funds either owed to you or sent by you, represents a moment of truth in the financial ecosystem.

The reasons behind receiving a check from Wells Fargo can be varied. Perhaps it's an insurance settlement, a tax refund, or a payment from a client or employer who prefers traditional methods. It could also be a personal check from someone who banks with Wells Fargo. Regardless of the reason, it's crucial to approach the situation with a clear understanding to ensure you handle the check correctly.

Navigating the world of checks might seem straightforward, but it's not without its nuances, especially in an era of increasingly sophisticated financial scams. Understanding the implications, potential pitfalls, and best practices associated with receiving a check from Wells Fargo is essential to ensure a smooth and secure financial experience.

While this article focuses on receiving checks from Wells Fargo, the information and advice provided can be broadly applied to any check you receive. It aims to empower you with the knowledge to navigate this aspect of personal finance confidently and securely.

Advantages and Disadvantages of Receiving a Check from Wells Fargo

| Advantages | Disadvantages |

|---|---|

|

|

|

|

Best Practices for Handling Checks

Here are five best practices to consider:

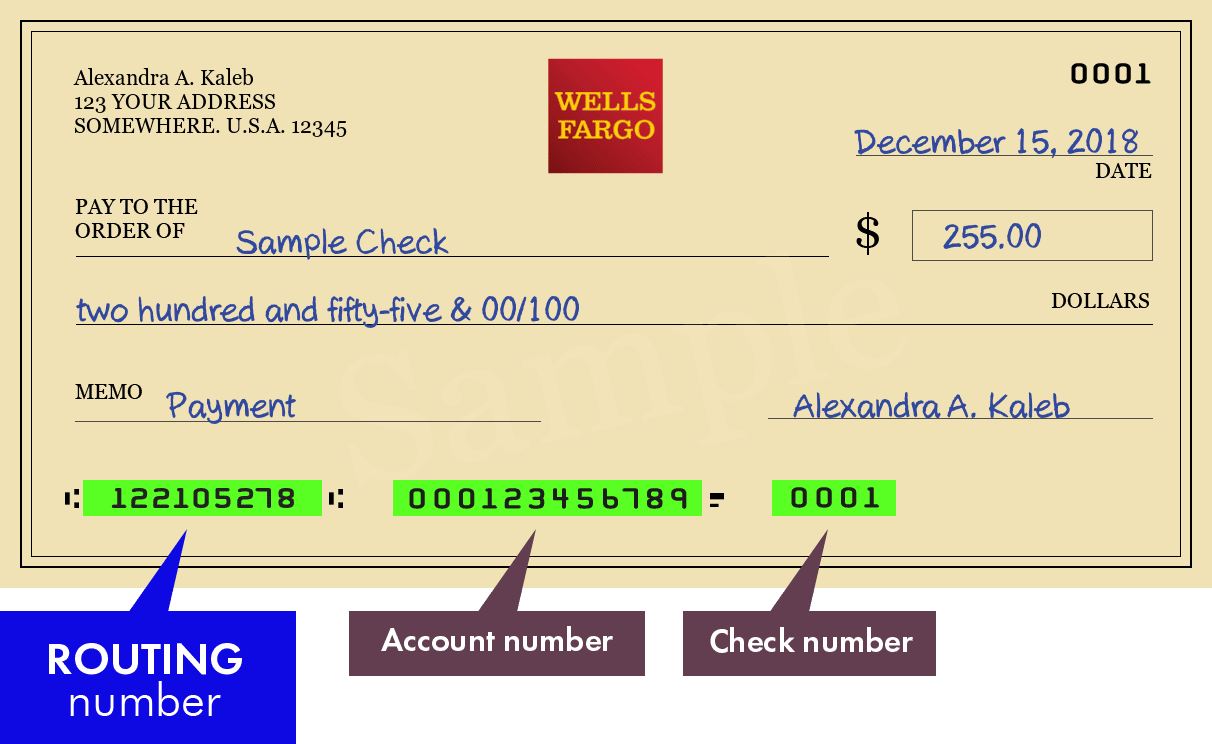

- Verification: Before depositing or cashing, verify the check's legitimacy. Look for security features, contact the issuer if unsure, and be wary of unsolicited checks.

- Timely Deposit: Deposit the check promptly to avoid potential issues like stop payments or delays in fund availability.

- Endorsement: Sign the back of the check (endorse it) only when you're ready to deposit or cash it, and ensure the signature matches your bank records.

- Record Keeping: Keep a record of the check, including the check number, amount, issuer, and the date you deposited or cashed it, for future reference.

- Security: Handle checks with care. Store them in a safe place, and shred them properly after they've been processed.

In conclusion, receiving a check from Wells Fargo, while seemingly a relic of the past, is still a relevant aspect of personal finance. While the convenience and speed of digital transactions dominate our financial landscape, understanding how to navigate the world of checks remains essential.

By embracing best practices, being aware of potential issues, and staying informed, you can confidently handle any financial instrument that comes your way, ensuring a smooth and secure financial experience. Remember, knowledge is key, and in the world of finance, an informed individual is an empowered individual.

Feeling better near you find biomat plasma therapy hours

Brown pennington atkins funeral home obituaries a comprehensive guide

Elevate your soundscape achieving audio nirvana on a budget

{kind=link}

/cloudfront-us-east-1.images.arcpublishing.com/gray/WNARNPX4URHZ3LW3PMKAADXGAU.jpg)

{kind=link}