Navigating Medicare AARP Supplement Plans

Healthcare decisions can feel like navigating a complex maze, especially as we age. The desire for financial security and quality medical care often leads individuals to explore supplemental insurance options. One prominent avenue for this is through AARP-endorsed Medicare supplement plans, offering a layer of protection to help manage out-of-pocket expenses. These plans, provided by UnitedHealthcare Insurance Company, can be a crucial piece of the healthcare puzzle, but understanding the nuances is essential for making informed choices.

Choosing a Medicare supplement plan requires careful consideration of individual needs and circumstances. It's about balancing peace of mind with budgetary considerations. Factors such as pre-existing conditions, expected medical utilization, and financial comfort levels play a significant role in determining the most appropriate coverage. With numerous plan options available, understanding the differences in benefits and premiums is key.

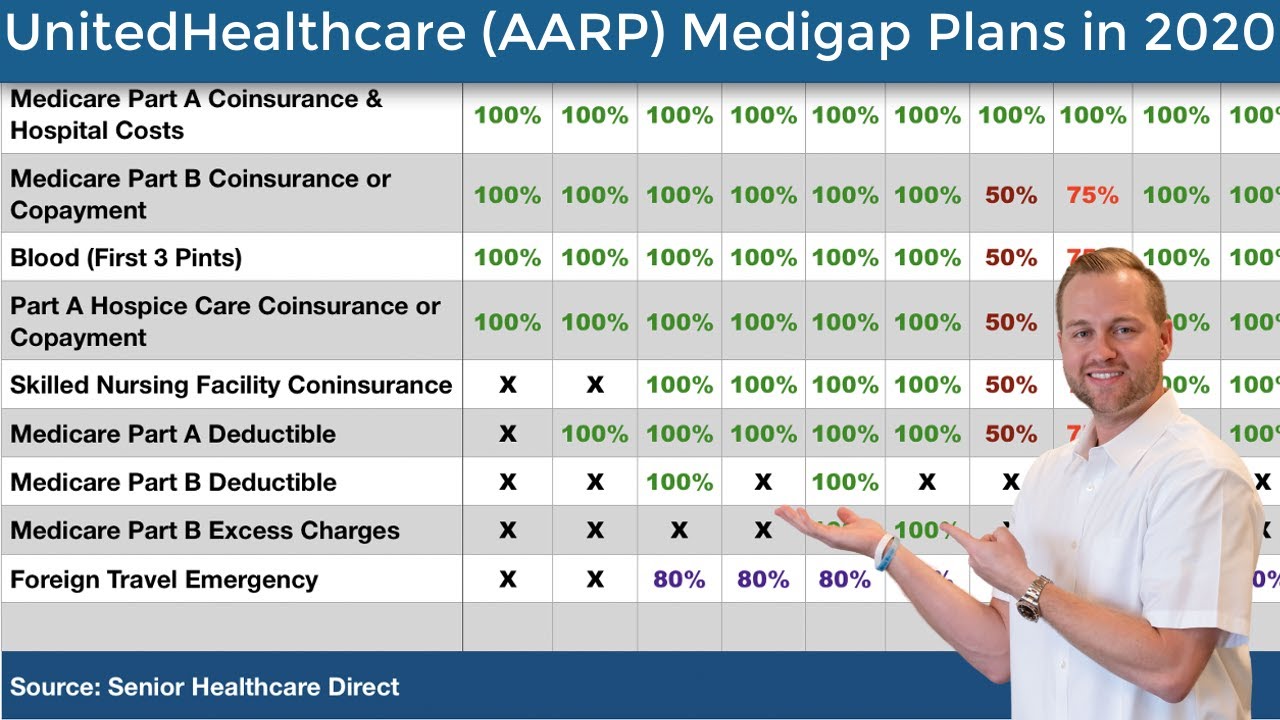

AARP Medicare supplements are standardized plans, labeled with letters (like Plan G or Plan N), each offering specific levels of coverage. These plans help cover costs that Original Medicare doesn't, such as copayments, coinsurance, and deductibles. This added financial buffer can prove invaluable in unexpected medical situations, providing a safety net against potentially high healthcare bills.

The history of Medicare supplemental insurance is intertwined with the evolving landscape of healthcare in the United States. As healthcare costs rose, the need for additional coverage became apparent, leading to the development of standardized Medigap plans. AARP, a prominent advocacy group for older Americans, recognized this need and partnered with UnitedHealthcare to offer these plans to its members. AARP does not offer the plans directly but endorses them; UnitedHealthcare is the insurer.

The importance of Medicare supplement plans lies in their ability to bridge the gaps in Original Medicare coverage. While Original Medicare provides valuable benefits, it doesn't cover everything. This can leave beneficiaries vulnerable to substantial out-of-pocket expenses. Supplemental coverage aims to minimize these costs, providing financial predictability and access to care without the worry of unexpected bills.

For example, if an individual undergoes a hospital stay, Original Medicare might cover a portion of the expenses, leaving the beneficiary responsible for a deductible and coinsurance. A Medicare supplement Plan G, for instance, could cover those remaining costs, significantly reducing the financial burden on the individual. Another example is Plan N, which offers similar coverage to Plan G but requires copays for doctor visits and emergency room visits. This option can be attractive for individuals seeking lower premiums.

Benefits of AARP Medicare supplement plans can include predictable healthcare costs, greater financial security, and access to a broader range of healthcare providers who accept Medicare. This can offer peace of mind and allow individuals to focus on their health and well-being without the constant worry of unexpected medical expenses.

When considering an AARP Medicare supplement, gather information about different plan options, compare premiums and benefits, and evaluate your individual health needs and budget. Talking to a licensed insurance agent specializing in Medicare can provide personalized guidance.

Recommendations: The official Medicare website (Medicare.gov) and the AARP website (AARP.org) offer valuable resources for understanding Medicare and supplement plans.

Advantages and Disadvantages of Medicare AARP Supplement Plans

| Advantages | Disadvantages |

|---|---|

| Predictable out-of-pocket costs | Monthly premiums |

| Coverage for Medicare cost-sharing | Can be more expensive than Medicare Advantage |

| Freedom to choose any doctor who accepts Medicare | May not cover all healthcare costs |

Frequently Asked Questions:

1. What is the difference between Medicare Advantage and a Medicare Supplement?

Medicare Advantage plans are an alternative to Original Medicare, while Medicare Supplements work alongside Original Medicare to fill coverage gaps. 2. What is the most popular AARP Medicare Supplement plan?

Plan G and Plan N are often chosen for their comprehensive coverage.

3. When can I enroll in a Medicare Supplement plan?

Typically, the best time is during your Medigap Open Enrollment Period.

4. Are there medical underwriting requirements for AARP Medicare Supplement plans?

During the Medigap Open Enrollment Period, you generally cannot be denied coverage based on pre-existing conditions. Outside of this period, medical underwriting may apply.

5. How do I find the best AARP Medicare Supplement plan for me?

Comparing plans, considering your healthcare needs and budget, and consulting with a licensed insurance agent can help you choose the right plan.

6. Can I switch AARP Medicare Supplement plans later?

You can switch plans, but you may be subject to medical underwriting.

7. What does AARP's endorsement of Medicare Supplement plans mean?

AARP endorses the plans, but UnitedHealthcare Insurance Company provides them.

8. What if I have questions about my AARP Medicare Supplement plan?

Contact UnitedHealthcare directly with questions regarding your specific plan.

In conclusion, navigating the landscape of Medicare and supplemental coverage can seem daunting. However, armed with the right information and resources, individuals can make informed decisions that align with their healthcare needs and financial goals. AARP Medicare supplement plans, offered by UnitedHealthcare, can play a significant role in ensuring financial security and access to quality care. Understanding the nuances of these plans, comparing options, and seeking professional advice are essential steps toward making the best choices for a healthy and secure future. Taking the time to thoroughly research and understand your options empowers you to navigate the complexities of healthcare with confidence and plan for a future where your health and well-being are well-protected. Remember, consulting with a licensed insurance agent specialized in Medicare can provide personalized guidance tailored to your specific circumstances.

Spice up your snaps using money emojis effectively

Bathroom bliss unveiling the tile mystery for your dream tub surround

Rainwashed by sherwin williams a deep dive into the soothing hue

{kind=link}